Are We Heading For Another Crash?

With the Coronavirus going around and the stock market tanking, people are wondering if we are headed for another real estate market crash like 2008. While I don't proclaim to know where the market will be in six months, comparing the current situation to 2008 is like comparing apples to oranges. Below are 5 key differences between 2008 and 2020.

1. Mortgage Standards Are Much Stricter Now

During the run up to the housing bubble, it was extremely easy to qualify for a mortgage. No doc loans were prevalent - if you could breathe, you could get a loan. A no doc loan was short for no documentation, meaning you didn't need to provide any documentation. Crazy, huh? Eventually the music stopped and all those people that were in over their heads in debt, couldn't simply sell their home to the next highest bidder. We are no where near that situation now.

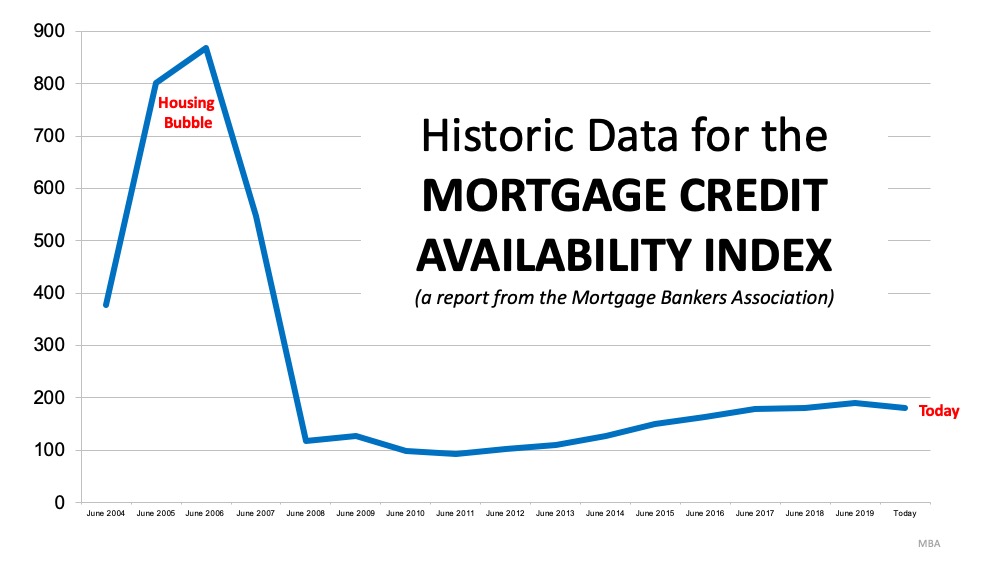

The Mortgage Bankers Association (MBA) issues a mortgage credit availability index. The higher the index, the easier it is to get a mortgage.

Mortgage Availability

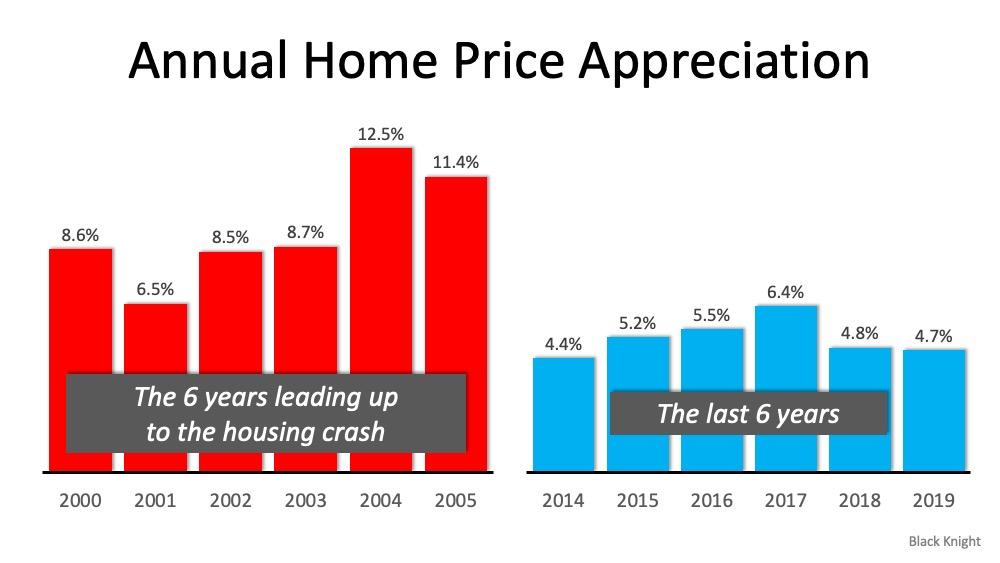

2. Home Price Appreciation Is Not What It Was

While prices have been rising here the past couple years, it is not like the run up in prices from 2003-2005. I was just getting started in my real estate career in 2003 and remember people camping out overnight to put a contract on a new condo building that wouldn't be delivered until the following year. People were buying new condos based on a floor plan and some slick marketing material. !

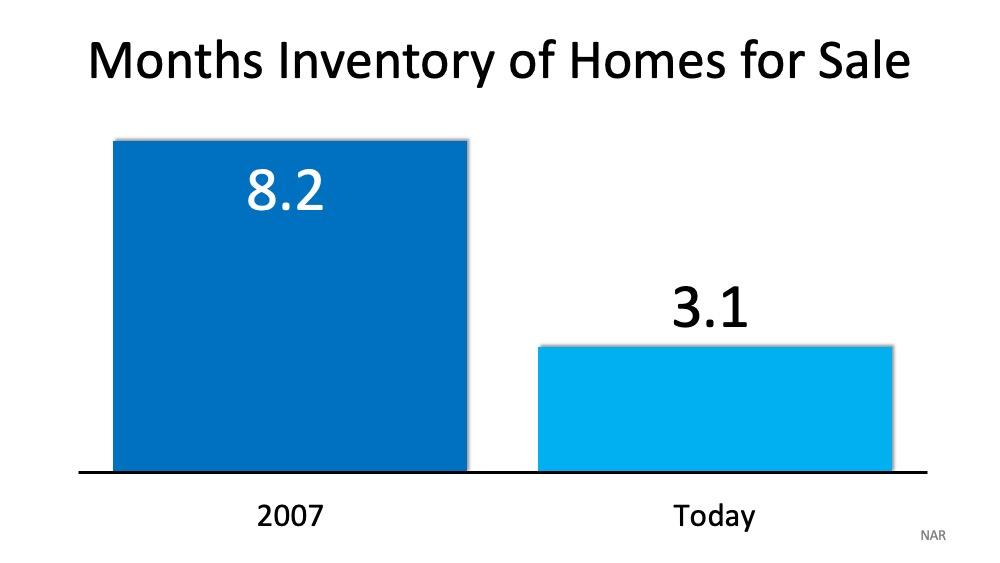

3. Inventory levels are vastly different.

Housing inventory is often measured in months of supply (based on the current sales pace, how long would the existing supply last if no new units came to the market). If you have been reading my newsletter the past year, you are probably tired of me reporting how low the inventory level is here. On a national level, inventory is around 3.1 months. For the Arlington condo market, the supply is less than 1 month and has been for a while.

A balanced market is around 5-6 months supply. When the supply gets higher than that, prices will decrease.

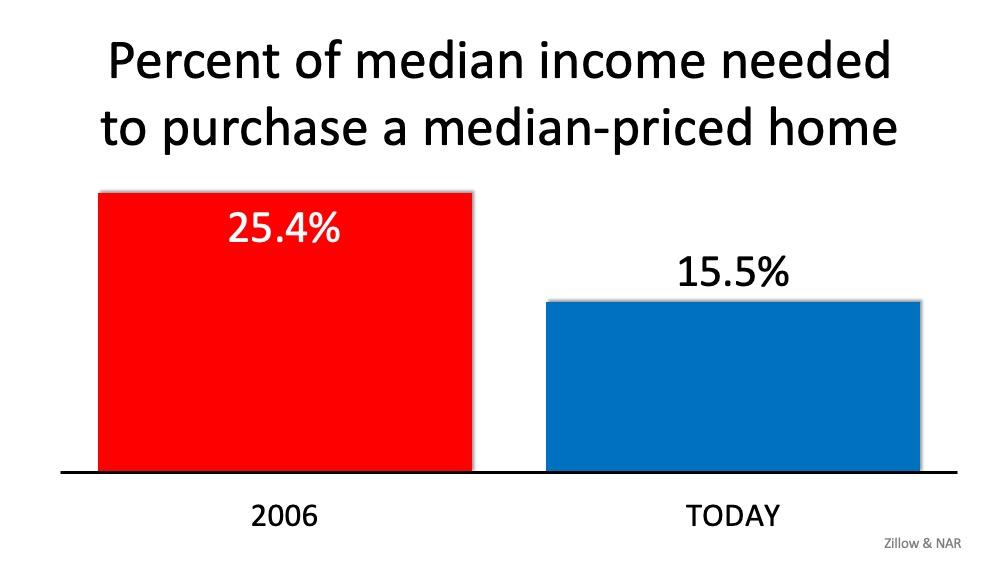

4. Houses Became Too Expensive

The housing affordability formula has three components: home prices, wages earned, and mortgage rates. Back in 2006, home prices were high, average wages were low, and mortgage rates were over 6%. Today, prices are still high, but wages are up and interest rates are low. That means the average household pays less of their monthly income towards their housing than they did in 2006.

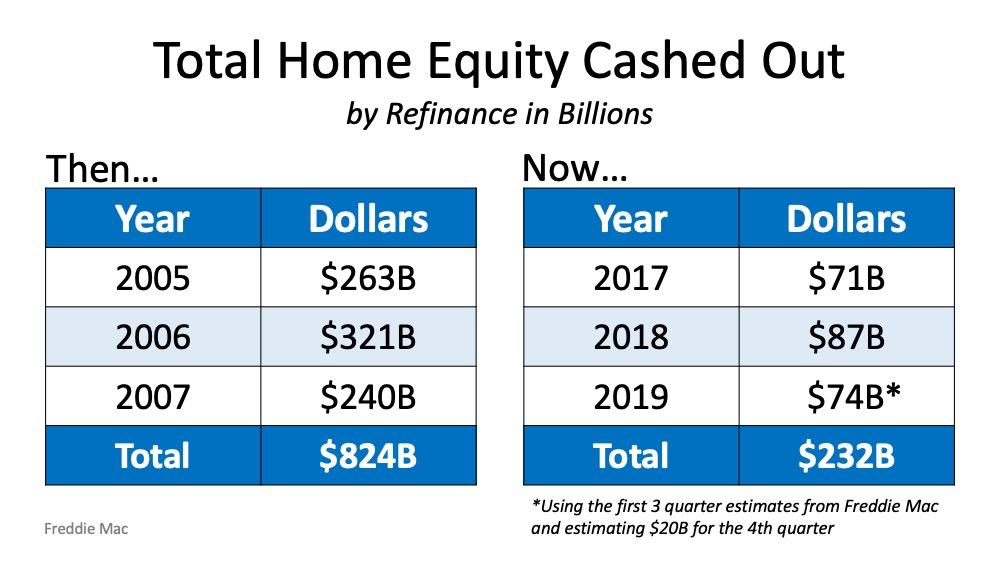

5. Homeowners Have Not Tapped Out Of Their Equity

Back then, mortgages were easy to get and it was easy to refinance and take cash out too. When homes appreciated 20% per year, it was too easy to refinance and take out some cash and buy that new boat or that trip to Hawaii.

Summary

We are in un-chartered territory with the Coronavirus and nobody really knows what is ahead for the real estate market. However, the situation is much different that during the housing bubble and financial crisis. There will be some disruption in the market but the fundamentals are solid and we will get through it.

{kind=link}

{kind=link}

{kind=link}