Mortgage Rates Are Melting

Their Grip on the Market

Back in 2023 and 2024, it seemed like every housing headline made the same point: homeowners were locked in by their low mortgage rates. People who refinanced or bought during the pandemic weren’t just lucky—they were sitting on loans they’d never want to give up.

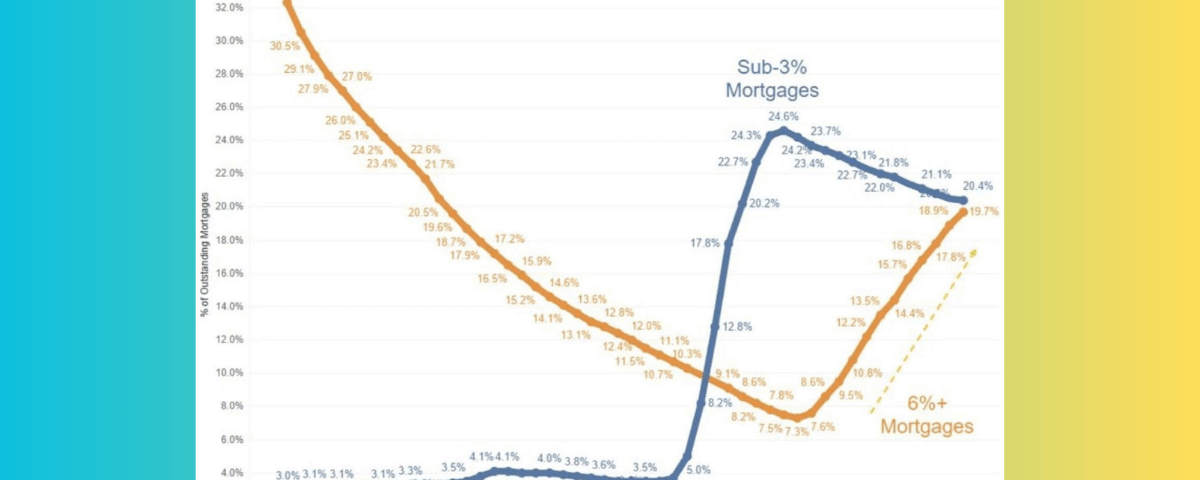

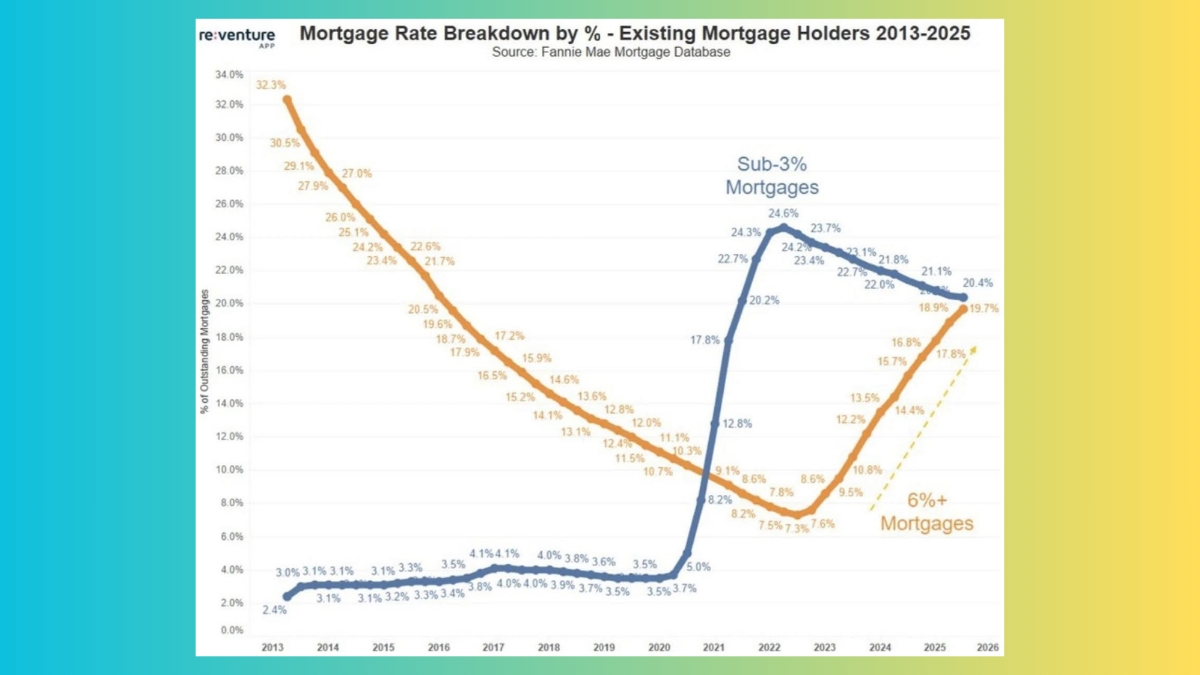

At the time, one stat stood out: 72% of all mortgages were originated below 4%. That massive wave of cheap money kept millions of owners rooted in place, unwilling to trade a 3% loan for one twice as high.

For many, moving simply didn’t make financial sense. Even a lateral move—say, from one condo to another—would have doubled their monthly housing costs once you factored in current mortgage rates. Still, life happens: marriages, divorces, growing families, job transfers. Some owners had to move, regardless of the math. And now, another factor is starting to surface—some of those ultra-low-rate loans were adjustable-rate mortgages (ARMs), and as they begin to reset, a few homeowners are rethinking their options.

But here’s the turning point: according to Fannie Mae’s latest data, we’re about to cross a major threshold. Within the next few months, there will be more mortgages above 6% than below 3%.

That shift doesn’t mean the market will suddenly loosen up, but it does signal a gradual thaw. As fewer homeowners are anchored by those ultra-low rates, more listings should start to appear. Over time, that could help ease the inventory crunch and move us closer to a more balanced, sustainable housing market.

More Mobility Ahead

As more homeowners lose their “rate lock” advantage, we’ll likely see a slow increase in mobility — people downsizing, moving closer to work or family, or trading up as equity builds. That means more choices for buyers and a bit more competition for sellers. The next phase of the housing cycle may be less about scarcity and more about balance.

Equity Has Been Building Fast

The silver lining for those who bought or refinanced at record-low rates is how much equity they’ve gained. With a lower interest rate, a greater portion of each monthly payment goes toward paying down principal rather than interest. That accelerated repayment, combined with years of rising home values, has created an enormous equity cushion.

Even if a homeowner’s next mortgage rate is higher, that equity gives them flexibility — and makes it easier to move when life calls for it.

A Shift in Mindset

After two years of “rate shock,” both buyers and sellers are adjusting to the new normal. Six-percent mortgages no longer sound outrageous — they’re just the market. As expectations reset and people refocus on lifestyle rather than rate, more homeowners will decide it’s time to make a move they’ve been putting off since 2022.

The Bottom Line

The freeze caused by ultra-low mortgage rates is beginning to thaw. It’s not a sudden flood of inventory, but a slow, steady drip that will open up more opportunities for both buyers and sellers — and move us closer to a balanced market where transactions happen for the right reasons, not just the right rate.

What It Means for Arlington Condo Buyers and Sellers

Here in Arlington, we’re already seeing early signs of this thaw. Condo listings that would have been delayed a year or two ago are coming to market as owners weigh their equity against lifestyle needs. For sellers, that means more competition — and the importance of pricing and presentation will only grow. For buyers, it means a little more breathing room and a few more choices.

It’s not a buyer’s market or a seller’s market — it’s becoming a balanced one. And that’s good news for everyone.

{kind=link}

{kind=link}

{kind=link}