Interest Rate - Condo Price Connection

Low interest rates, while often seen as a driver of real estate transactions, can also discourage homeowners from selling their properties. Many owners secured their homes during a period of historically low mortgage rates. These favorable rates made owning a home more affordable by reducing monthly mortgage payments. If they were to sell, they would likely face much higher interest rates when purchasing a new home, leading to significantly higher monthly payments. This "rate lock-in" effect causes homeowners to think twice about selling, as it becomes financially less appealing to move, even if their current home no longer suits their needs.

Additionally, many homeowners refinanced their mortgages during low-rate periods, locking in favorable terms for the long term. Selling and repurchasing under current higher interest rates means potentially losing those advantages. This creates a situation where homeowners feel "stuck" in their current properties, reducing inventory in the housing market and limiting options for buyers. The fear of higher costs deters many from making a move, even if they might otherwise be inclined to sell.

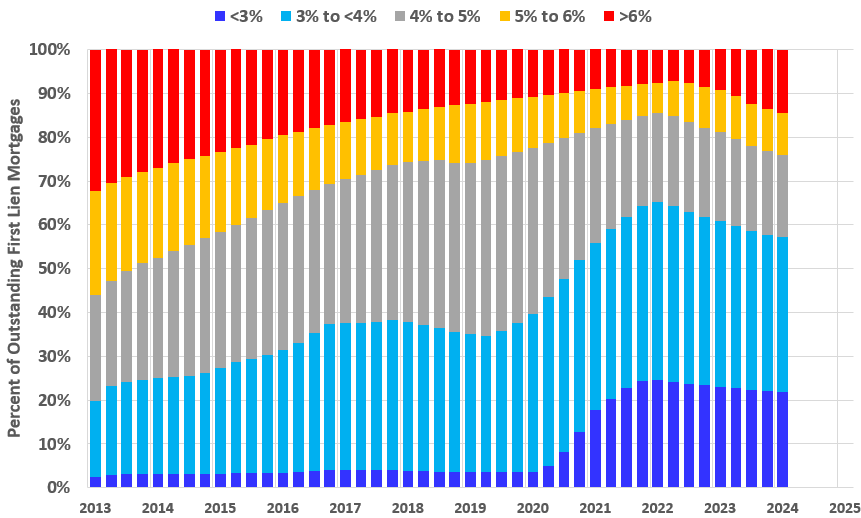

The graphic above illustrates the problem precisely. Roughly 20% of homeowners across the nation that have a mortgage, have a rate under 3% (purple). Another 40% have a rate between 3-4% (blue). Combined, that means 60% of homeowners with a mortgage have a rate under 4.0%.

Fed Rate Cut

In case you didn’t hear the big news from the Fed, on Wednesday the Fed cut its benchmark interest rate by a half point, which was larger than expected. However, don’t expect mortgage rates to drop by a half percent.

The anticipation of rate cuts has already contributed to a drop in mortgage rates, even before the Fed's official announcement on Wednesday. Currently, long-term fixed-rate mortgages are sitting at around 6.2%, the lowest they've been since February 2023. However, it’s important to note that mortgage rates are influenced by more than just the Federal Reserve’s benchmark rate; broader economic factors also play a role. This suggests that the recent rate cut may have already been factored into the current mortgage rates, though further declines are likely as the Fed signals more rate cuts into next year.

Impact for buyers

The impact for buyers will be mixed. Their buying power will increase, but that could lead to higher demand and an increase in prices. How much more buying power will a buyer have? One way to look at it is to work backwards starting with a certain mortgage payment (column on the left) and see what loan amount that equates to at various interest rates.

| Payment (monthly) | Interest Rate | ||||

|---|---|---|---|---|---|

| 5.50% | 5.75% | 6.00% | 6.25% | 6.50% | |

| $1,000 | $176,121 | $171,358 | $166,791 | $162,412 | $158,210 |

| $1,500 | $264,182 | $257,037 | $250,187 | $243,618 | $237,316 |

| $2,000 | $352,243 | $342,716 | $333,583 | $324,824 | $316,421 |

| $2,500 | $440,304 | $428,395 | $416,979 | $406,030 | $395,527 |

| $3,000 | $528,365 | $514,074 | $500,374 | $487,236 | $474,632 |

| $3,500 | $616,426 | $599,753 | $583,770 | $568,442 | $553,737 |

| $4,000 | $704,487 | $685,432 | $667,166 | $649,648 | $632,843 |

| $4,500 | $792,547 | $771,111 | $750,562 | $730,855 | $711,948 |

| $5,000 | $880,608 | $856,791 | $833,958 | $812,061 | $791,054 |

Often when we talk about mortgage payments and interest rates, we start with the loan amount and interest rate to calculate the payment. For example, for a $400,000 loan at 6.25% interest rate over 30 years, the payment would be $2,462 per month.

The table above starts with a set payment amount in the left column and increasing interest rates in the remaining columns.

For example, for a monthly payment of $3,000 (this is the principle + interest payment and doesn't include taxes, insurance or condo fees) at a rate of 6.5%, that would get you a loan of $474,632. At 5.5%, that same $3,000 payment would get you a loan of $528,365.

Is your head spinning by all the numbers? Do you have questions about your situation? Ask away.

{kind=link}

{kind=link}

{kind=link}