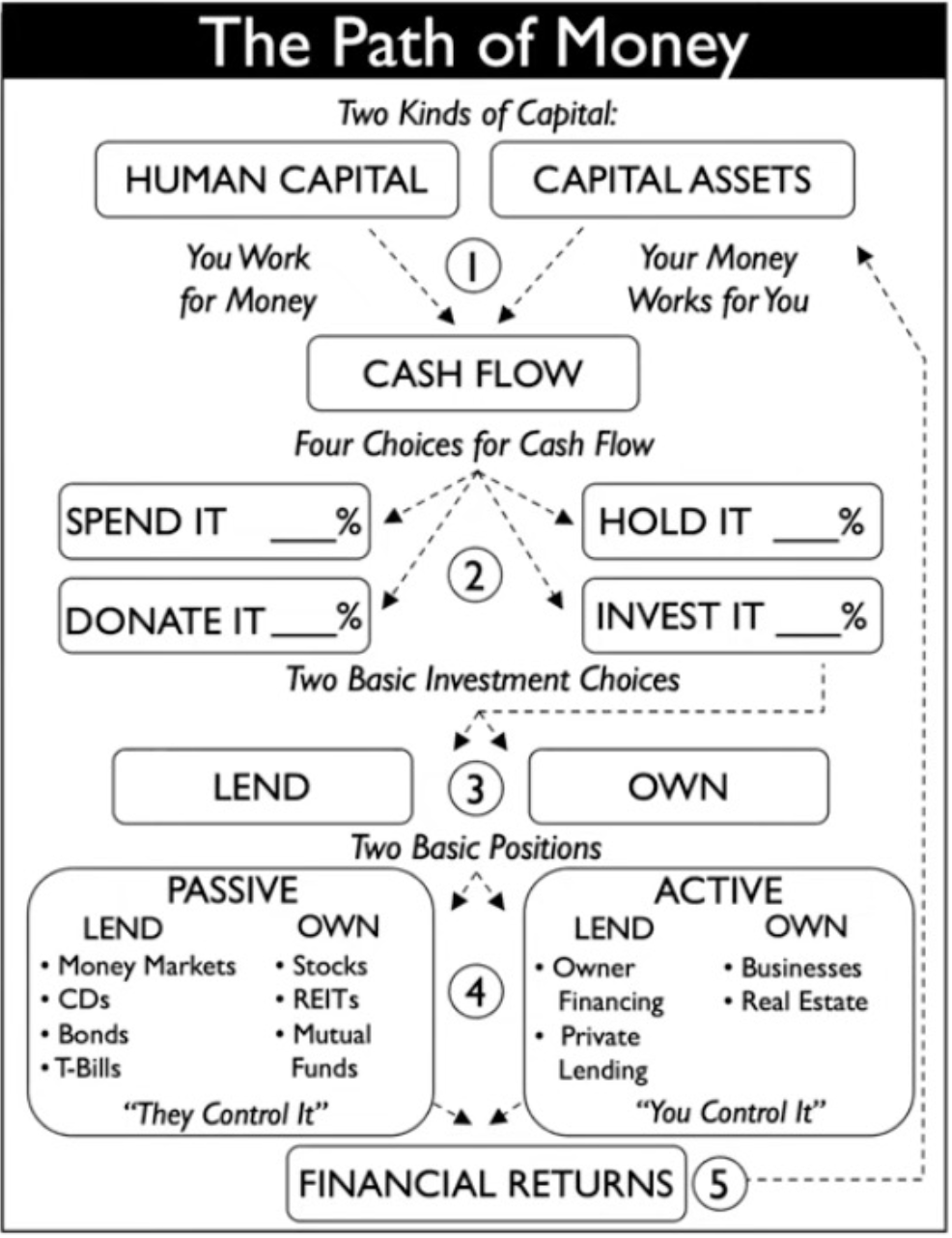

The Path Of Money For Wealth Building

Most of us are trying to build wealth using financial frameworks that just don't work. They're either way too complicated to follow or so basic they're useless. It's like trying to navigate new territory with either a rocket scientist's control panel (that we can't figure out) or a crayon-sketched treasure map.

What we really need is a clear, simple system that actually works. That's exactly what The Path of Money delivers.

The Simple Formula for Building Wealth

In order to build wealth, you need to earn money, save some, and then invest those savings. There are two basic ways to earn money. The first is trading your time for income. The second is what happens after you invest your savings and your money grows through appreciation or dividends.

Human Capital

You work for money.

This is the most familiar path for most people. You trade your time, skills, and energy in exchange for a paycheck. Whether you’re working a 9-to-5 job, running your own business, freelancing, or hustling on the side, you’re actively putting in effort to earn income. The downside? There are only so many hours in a day, and eventually, your ability to work may slow down or stop altogether. Relying solely on earned income keeps you on the treadmill—if you stop working, the money stops coming in.

Capital Assets

Your money works for you.

The Four Things You Can Do With Money

Once you’ve earned money, every dollar has four possible jobs - spend it, donate it, save it, or invest it. How you divide your money across these choices ultimately shapes your financial future.

Spend

Spending is the most immediate and familiar use of money. This covers both your essentials—like housing, food, transportation, and taxes—and your non-essentials, like dining out, travel, entertainment, and hobbies. Spending isn’t inherently bad (we all need to live and enjoy life), but without intention, it’s easy for spending to consume everything you earn, leaving nothing behind for the other, more productive uses of money.

Donate

Giving money away—whether to charities, causes, or people you care about—might not seem like a wealth-building move, but it plays a powerful role in your mindset. Donating helps create a sense of abundance, signaling to yourself that you have more than enough. It keeps money in perspective and can deepen your sense of purpose and connection to your community. Plus, giving can come with tax benefits depending on how and where you give.

Save

Saving is about safety and security. This is the money you set aside for emergencies, unexpected expenses, and short-term goals. A healthy savings cushion prevents financial stress and keeps you from going into debt when life throws you a curveball. But while saving is crucial, it’s not the end goal—because money sitting in a savings account isn’t growing much. Saving is the holding zone before money moves into the next, most important job: investing.

Invest

Investing is where money starts to work for you. It’s how you build long-term wealth and create income streams that don’t rely on your daily effort. Whether you’re investing in stocks, real estate, businesses, or other assets, the goal is to grow your money over time. Unlike saving, which protects what you have, investing multiplies it. The more you can move from spending to saving, and from saving to investing, the faster you accelerate your path to financial freedom.

Understanding the Four Types of Investments

All investments fall into two main approaches: Passive or Active. From there, they can be further divided into whether you're Lending your money or Owning assets. This simple framework helps you understand how much effort is required and what kind of returns you can expect.

Passive

Passive investments are designed to work in the background with little to no involvement from you. These are typically set-it-and-forget-it strategies with modest returns and lower risk.

Active

Active investments require your time, energy, and decision-making. In exchange for more work, you have the potential to earn higher returns.

Passive Lending

You’re letting others use your money with minimal oversight. Common examples include:

- savings accounts

- CDs and

- bonds.

Returns are generally low—around 0–4%—but these options are very hands-off and stable.

Passive Ownership

You own assets without actively managing them. This includes investments like:

- stocks

- index funds

- mutual funds and

- REITs.

Historically, these produce higher returns than passive lending—usually around 8–12%—while still being relatively hands-off.

Active Lending

Here, you’re directly involved in lending, such as:

- providing private loans

- offering owner financing on properties.

- buying or selling notes

You manage the terms, the borrower, and the risk, with potential returns in the 8–15% range.

Active Ownership

This is the most involved investment type, where you're running or managing the asset yourself like:

- real estate rentals

- house flips or

- owning and operating a business.

Active ownership takes real effort but offers the highest potential rewards—typically 13% and up.

Why Expectations and Strategies Don't Always Match

This is where most people go wrong: They expect active investment returns from passive investments. This creates a gap between our expectations and our strategies. And it's the reason so many of us feel perpetually behind on our wealth-building journey.

How Fast Can Your Money Grow?

The Rule of 72 is a great way to understand how money compounds at different rates. Divide 72 by your expected rate of return to see how many years it takes for your money to double:

- At 4% (passive lending), your money doubles about every 18 years.

- At 8% (passive investing), your money doubles about every 9 years.

- At 12% (active lending), your money doubles about every 6 years.

- At 18% (active ownership), your money doubles about every 4 years!

Why Investment Type Matters More Than You Think

The difference between 8% and 12% isn't just about 50% more annual return—it's the difference between your money doubling every 9 years versus every 6 years. Over a 30-year period, $10,000 growing at 8% becomes $100,627. At 12%, it becomes $299,599. That's more than a 3X difference!

Shifting Your Strategy for Bigger Results

You don’t need to quit your job and become a full-time investor overnight. But it’s important to recognize where your current investments fall within this framework—and consider ways to gradually shift more of your money from passive to active, and from lending to ownership.

For some, that might look like buying a rental property. For others, it could mean finally launching that side business you've been thinking about. The goal isn’t to take on more risk just for the sake of it, but to intentionally move toward investments that have the potential to create higher returns and build lasting wealth.

{kind=link}

{kind=link}

{kind=link}