Who Really Sets Mortgage Rates?

(Hint: Not the Fed)

If you’ve been following financial news, you’ve probably noticed the headlines about the Federal Reserve raising or lowering interest rates. But here’s the question most condo buyers and sellers ask: Does the Fed control mortgage rates directly?

The short answer is: not exactly.

The Fed Funds Rate

The Federal Reserve sets the Federal Funds Rate, the short-term interest rate banks charge each other for overnight loans. Think of it as the cost of money for banks. When the Fed raises this rate, it becomes more expensive for banks to borrow, and that higher cost often ripples through the economy.

The 10-Year Treasury Bond

Mortgage rates don’t follow the Fed Funds Rate directly. Instead, they track closely with the 10-year Treasury bond yield. Why? Investors see 10-year Treasuries as one of the safest investments. When those yields rise, lenders need to offer higher returns on mortgages to compete, which pushes mortgage rates higher.

Mortgage Rates

So while the Fed influences the broader economy and investor sentiment, it’s the 10-year Treasury yield that’s the key driver for mortgage rates. For example, if investors expect inflation to rise, they demand higher yields on Treasuries, and mortgage rates climb as a result—even if the Fed doesn’t make a move that day.

Key Differences at a Glance

- Federal Funds Rate (FFR):

- The Fed’s main monetary policy tool.

- Reflects the rate banks charge each other for overnight loans.

- Has the most direct impact on other short-term interest rates.

- 10-Year Treasury Yield:

- Driven by investor demand and economic confidence.

- Falls when demand for safe-haven assets is high; rises when confidence is strong.

- Influenced by inflation expectations, growth outlook, and geopolitical risk.

- Impacts longer-term borrowing costs, including fixed-rate mortgages and corporate debt.

- Yield Curve & Signals:

- The relationship between short- and long-term rates (the yield curve) can send signals about the broader economy.

- Investors watch the curve for insights into future growth, inflation, and market sentiment.

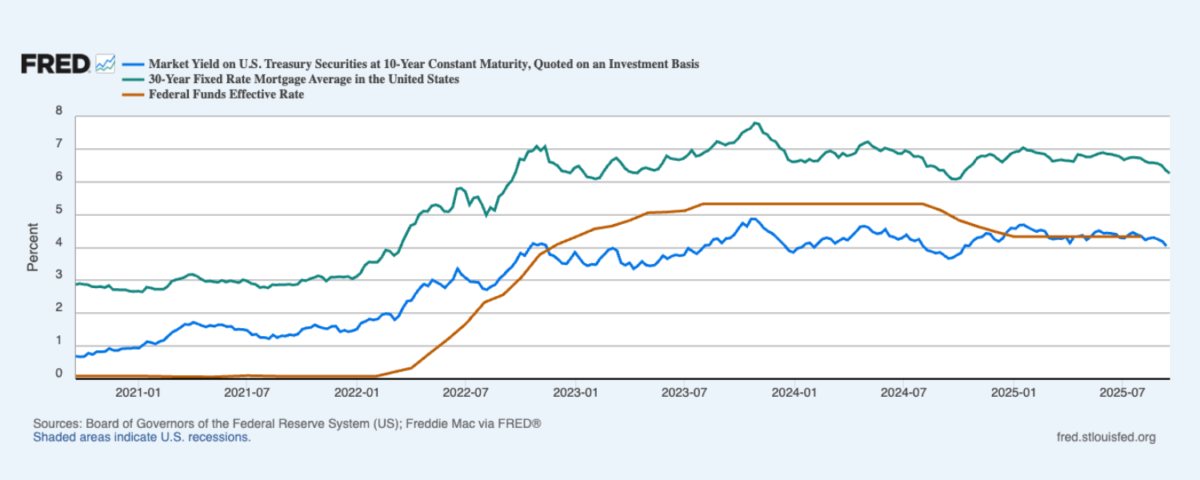

What the Chart Shows (2020–2025)

- Early 2020–2021: The Fed Funds Rate (red) was near zero. Mortgage rates (green) and Treasury yields (blue) were also historically low, fueling a hot housing market.

- 2022–2023: As inflation surged, the Fed raised the Funds Rate aggressively. Treasury yields spiked, and mortgage rates followed—jumping from the 3% range to over 7% in just over a year.

- 2024: Even when the Fed held rates steady, Treasury yields and mortgage rates bounced around depending on inflation data and investor sentiment. Notice how the blue (10-year) and green (mortgage) lines move almost in tandem.

- 2025: When the Fed began cutting rates, mortgage rates eased slightly, but not nearly as much as the Fed Funds Rate. This highlights that mortgages respond more to market expectations than to Fed policy alone.

Why This Matters for Buyers & Sellers

- For buyers: Mortgage rates are more tightly linked to the 10-year Treasury yield than the Fed’s announcements. That’s why you’ll often see rates rise or fall before the Fed even meets.

- For sellers: Higher mortgage rates can shrink the buyer pool, while lower rates can increase affordability and bring more buyers to the table.

Frequently Asked Questions

📌 Does the Fed directly set mortgage rates?

No. The Fed sets the Federal Funds Rate, which influences short-term borrowing costs. Mortgage rates move more closely with the 10-year Treasury yield.

📌 Why do mortgage rates track the 10-year Treasury?

Because most homeowners keep their mortgages for around 7–10 years, lenders use the 10-year Treasury yield as a benchmark when pricing loans.

📌 If the Fed cuts rates, will my mortgage rate drop?

Not always. Mortgage rates depend more on investor expectations for inflation and growth than on Fed policy changes alone. Sometimes mortgage rates even rise while the Fed is cutting.

📌 What does this mean for buyers and sellers?

For buyers, affordability hinges on Treasury yields as much as Fed moves. For sellers, shifts in mortgage rates can expand or shrink the pool of qualified buyers.

The Bottom Line

The Fed Funds Rate sets the tone, but the 10-year Treasury bond does the heavy lifting when it comes to mortgage rates. The chart makes it clear: mortgage rates follow the Treasury yield closely, not the Fed line-by-line. If you’re planning to buy or sell a condo in Arlington, keeping an eye on the 10-year yield can give you a good idea of where mortgage rates are headed.

{kind=link}

{kind=link}

{kind=link}